- The Site is maintained and operated by a third-party vendor, Citrix Systems, Inc. (the “Vendor”), a company that is not affiliated with Ingalls & Snyder, LLC (“Ingalls”). While Ingalls has selected the Vendor based on its belief that the Vendor has commercially reasonable safeguards designed to (i) ensure the security and confidentiality of any non-public information (“Information”) transmitted using the Site, (ii) protect against any anticipated threats or hazards to the security or integrity of Information transmitted using the Site and (iii) protect against unauthorized access to, or use of, Information transmitted using the Site, Ingalls does not exercise any control over the Vendor’s systems and cannot guarantee the privacy and security of any information you choose to transmit using the Site.

- Access to the Site is granted by Ingalls so that you may utilize the Service for your convenience at your sole discretion. Ingalls has no liability for any loss, claim, or other damage that results from unauthorized access to any Information transmitted using the Site. User is solely responsible for the security of Information stored locally on the User’s computer or device as well as any email account User may use to receive and send links to the Site to transmit or receive documents.

Current Market Commentary, March 2026

We are highly attuned, as are our readers, to the escalating hostilities in the Middle East. As investment managers, we continuously evaluate alternative courses of action, both in periods of calm and in periods of crisis. To date, we have not sought to dodge or deflect market price declines triggered by war. Circumstances may change, of course, and compel us to adapt our views. Based on what we understand today, however, we do not believe that abrupt defensive measures would benefit the long-term expected returns of equity and bond portfolios.

We entered 2026 confident in the prospective earnings growth of our portfolio holdings and their ability to compound long-term returns at attractive rates. We remain confident on this score. Recent portfolio changes have aimed to optimize portfolio outcomes by capitalizing on market discounts not dependent on either war or peace. We have remained patient buyers of high-quality, highly-liquid and attractively-valued assets.

We also entered 2026 in the knowledge that, inevitably, something will go wrong. It is imperative, at all times, that we manage portfolio risk. The primary risk which we monitor is that of a permanent impairment of asset values. In recent months, growing concern over the competitive threats posed to many businesses by artificial-intelligence (AI) resulted in steep valuation discounts across the software and data services industries. It remains unclear as to whether the share prices of many large companies will recover their former highs.

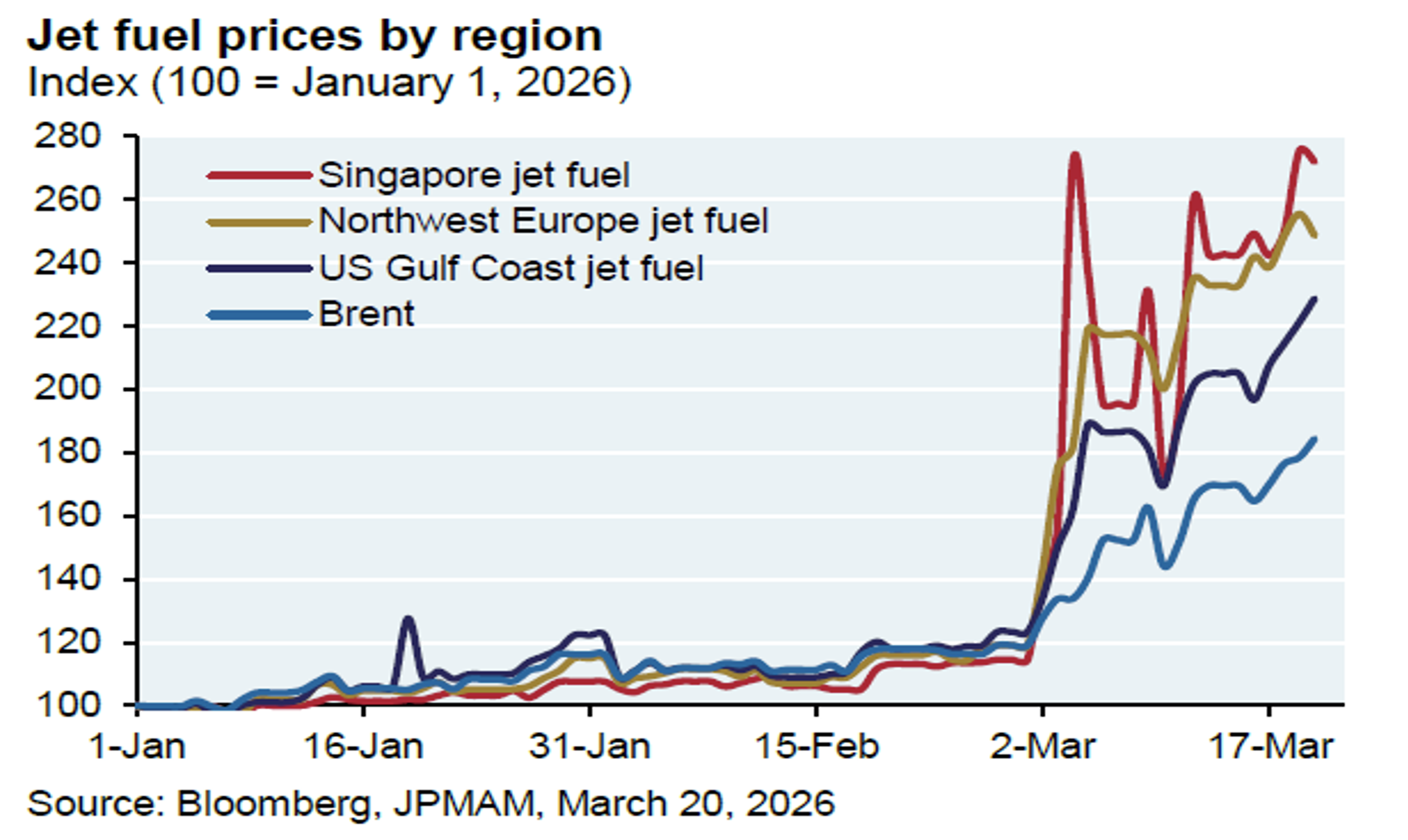

The war introduces a host of new risks, and which are primarily associated with a surge in energy prices, along with supply chain friction and reduced supply of fertilizer.

A prolonged energy price shock could negatively impact expected earnings growth for a broad set of industries and companies. It could even upend the economic models of many countries. A rise in borrowing costs and restricted demand raise the risk of economic recession.

Given fresh damage to oil and gas infrastructure and the fraught situation in the Strait of Hormuz, one should expect global energy and related commodity prices to remain elevated for some time – even if the war winds down and oil prices retreat from their recent peaks.

As public attention stays riveted on the unfolding hostilities and escalating threats, we are mindful of the hazards involved in making portfolio changes based on news clips and social-media messages. The military paradigm of “escalate to de-escalate” certainly raises the possibility of a deeper and broader conflict. At the same time, incentives to bring conflict to a close are also very high. Those who presume to trade based on conviction that the war can only get worse put themselves at risk of a single contrary headline or post on social media.

Amid the turmoil, we monitor portfolio holdings for potential negative impacts. We are equally attentive to investment opportunities. Ironically, the United States market and economy may benefit from their safe haven status due to abundant energy production, the relatively low energy-dependence of its large tech sector, as well as currency dominance. Already, certain assets and industries may be overly-discounted given limited exposure to energy and war-related risks. Nor have all sectors and stocks performed badly. Hostilities have boosted the share prices of energy and western fertilizer producers.

In the event of a major drawdown in market prices, we depend greatly on the quality and liquidity of portfolio assets. Market declines, while uncomfortable, provide scope to buy great assets at reduced prices. For portfolios designed to mitigate equity-market shortfalls and provide income, we are actively purchasing top-quality bonds at attractively discounted prices. Bond prices are sensitive, of course, to changing inflation expectations. For both equity and bond portfolios, we believe that it is wise to balance the high strains of the moment with a more moderate view of future outcomes.

We are grateful for the confidence you have placed in our abilities. We welcome your observations and questions, as always.

Sincerely,

Bridgehampton Group

For questions or follow-up, please reach out to any member of our team. https://www.ingalls.net/bridgehamptongroup/about-us

Ingalls & Snyder, LLC, is an investment advisor registered with the U.S. Securities & Exchange Commission and a FINRA member broker dealer. This material is being provided to you for informational purposes only and is not intended to be a general guide to investing, or as a source of any specific investment recommendation and makes no implied or express recommendation concerning the manner in which any account should be handled. Any investment program involves certain risks, including loss of principal, and no assurance can be given that any specific investment objective will be achieved.

Ingalls & Snyder is a brand name used for the affiliated companies of I&S Group, LLC. Bridgehampton Group is a team at Ingalls & Snyder that offers investment advisory and brokerage services. Investment advisory services are offered through Ingalls Investment Management, LLC ("IIM"), an SEC registered investment adviser, and brokerage services are offered through Ingalls & Snyder, LLC ("INGS"), a member of FINRA and SIPC. When offering investment advisory services, individuals act as investment advisor representatives or, otherwise, employees of IIM. When offering brokerage services, individuals act as a registered representatives or associated persons of INGS.

For more information and disclosures regarding Ingalls & Snyder, LLC and Ingalls Investment Management, LLC, please visit the Important Information page. In addition, you may check Ingalls’ regulatory history and background on FINRA’s BrokerCheck website.