- The Site is maintained and operated by a third-party vendor, Citrix Systems, Inc. (the “Vendor”), a company that is not affiliated with Ingalls & Snyder, LLC (“Ingalls”). While Ingalls has selected the Vendor based on its belief that the Vendor has commercially reasonable safeguards designed to (i) ensure the security and confidentiality of any non-public information (“Information”) transmitted using the Site, (ii) protect against any anticipated threats or hazards to the security or integrity of Information transmitted using the Site and (iii) protect against unauthorized access to, or use of, Information transmitted using the Site, Ingalls does not exercise any control over the Vendor’s systems and cannot guarantee the privacy and security of any information you choose to transmit using the Site.

- Access to the Site is granted by Ingalls so that you may utilize the Service for your convenience at your sole discretion. Ingalls has no liability for any loss, claim, or other damage that results from unauthorized access to any Information transmitted using the Site. User is solely responsible for the security of Information stored locally on the User’s computer or device as well as any email account User may use to receive and send links to the Site to transmit or receive documents.

2Q 2025 Investor Update

2025 year-to-date highlights

- Foreign equities drove strong returns in the 1st half of 2025

- Eurozone equities (Stoxx 50) +24.0% in US$

- US equities (S&P 500) +4.4% - though strengthening in June-July

- Risk aversion, policy shifts and speculative interest drove gains in foreign currencies, precious metals and bitcoin

- Swiss Francs +14.9%, Euros +12.9% versus the US$

- Gold +25.9%, silver +33%, Bitcoin +14.8%

Global investment opportunities

Following an extended period of US equity dominance, foreign equity markets generated superior returns in the first half of 2025. The strong recent performance of European and Asian markets is striking.

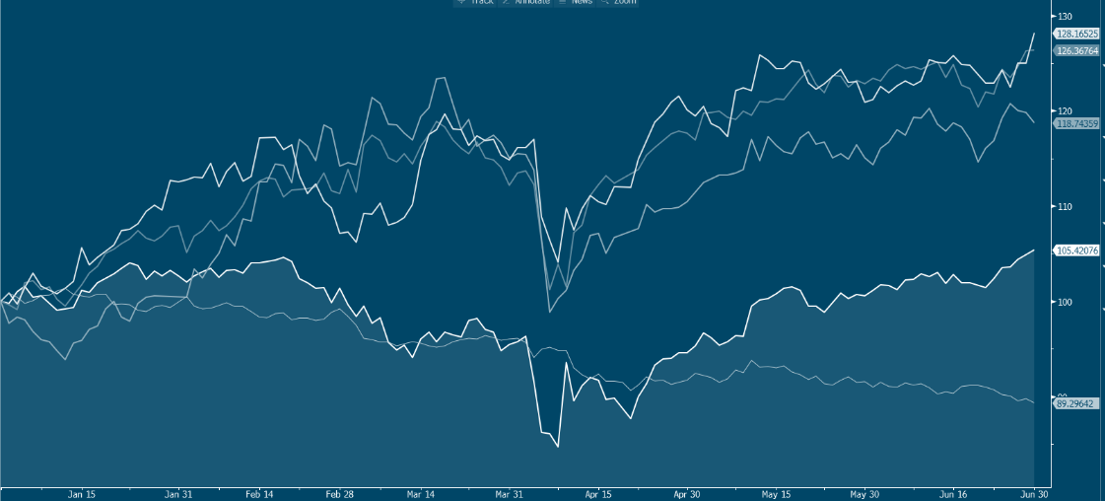

1st half 2025 equity market & US dollar returns

This chart should be interpreted with long-term perspective. Historically, US market returns have compounded at rates well above those of other markets. A 6-month period of non-US strength could easily prove to be an anomaly in an exceptional long-run track-record. In June and July, US markets outperformed foreign markets, as large tech stocks, industrials and financial shit new highs. Moreover, half of this year’s European and Asian equity returns in US$ owe to currency strength - a less reliable source of investment return than profit growth. Weakness in the dollar, all else equal, also boosts profits of US exporters and multinationals. Conversely, dollar weakness negatively impacts cash flows of foreign exporters and multinationals with large revenues generated in the US.

Yet we are also mindful that during relatively long periods, including much of the 1970s and 2000s, US equities underperformed foreign assets. During such periods, US$ portfolio returns were supported by diversification in foreign assets and currencies. Though an important factor in year-to-date investment returns, currency changes are not the sole source of foreign equity returns in2025. The recovery of growth in specific foreign sectors has revived invest or interest.

One such growth opportunity has emerged in the European defense sector. Soaring share prices of European defense and aerospace companies reflect a European commitment to substantially higher defense spending.

For decades, European countries counted on exports and tourism for growth – along with regulations to set standards and restrict foreign competition. Pressured by the US, as well as Russia and China, Europe is finally raising capital to invest in its domestic growth. Germany's €1 trillion stimulus package, passed in March, displayed a heightened sense of urgency with respect to both defending Europe’s borders and creating jobs for the German population. The order backlogs of French British, Italian as well as German defense and infrastructure firms have greatly increased in the past year. These backlogs will support hiring and training; they will also result in orders for materials and parts from suppliers in Europe and elsewhere. Investors rightly anticipate the start of a important investment cycle.

The Euro and European capital markets stand to benefit. Funding Germany’s €1 trillion fiscal package requires repatriation of foreign capital alongside large-scale issuance ofEuro-denominated debt. This, in turn, should help deepen and liquify relatively shallow European markets. The fraught debate between Europe’s national interests and the EU’s supra-national authority will likely intensify. In our view, external pressures make Europe’s financial integration more likely to occur than at any time since the 2001 launch of the Euro.

None of the above needs to come at the expense of the US economy and markets. Sustained weakness in the US dollar should benefit many US firms who export services and goods and who maintain large overseas operations. In the context of US tariffs and unfavorable US$ rates, many foreign firms will choose to further align their cost base with US-sourced revenue by expanding their US operations. The recently approved US tax bill provides them with additional incentives.

Portfolio Decisions

For over a decade we have managed dedicated foreign-equity investment strategies.We also believe that USD-based portfolios benefit from selective investment in non-US holdings. These provide an expanded palette of high-quality investments, as some of the world’s leading businesses are domiciled outside of the US. Investment opportunities in these markets are often overlooked, given a global preference for the larger, more liquid and more widely covered US markets. Two of our most recent purchases targeted Europe-based companies with major presences in the US and in Asia.

We are grateful for the confidence you place in our abilities. We welcome your observations and questions, always.

Ingalls & Snyder, LLC, is an investment advisor registered with the U.S. Securities & Exchange Commission and a FINRA member broker dealer. This material is being provided to you for informational purposes only and is not intended to be a general guide to investing, or as a source of any specific investment recommendation and makes no implied or express recommendation concerning the manner in which any account should be handled. Any investment program involves certain risks, including loss of principal, and no assurance can be given that any specific investment objective will be achieved.

Ingalls & Snyder is a brand name used by affiliated companies of I&S Group, LLC. Brokerage services are offered through Ingalls & Snyder, LLC (“INGS”), a FINRA and SIPC member, and advisory services are offered through Ingalls Investment Management, LLC (“IIM”), an SEC-registered investment adviser. Individuals provide brokerage services as registered representatives of or associated persons of INGS, and advisory services as investment adviser representatives or employees of IIM.

For more information and disclosures regarding INGS and IIM , please visit the Important Information page. In addition, you may check INGS’ regulatory history and background on FINRA’s BrokerCheck website.

Check the background of this firm on FINRA's BrokerCheck