- The Site is maintained and operated by a third-party vendor, Citrix Systems, Inc. (the “Vendor”), a company that is not affiliated with Ingalls & Snyder, LLC (“Ingalls”). While Ingalls has selected the Vendor based on its belief that the Vendor has commercially reasonable safeguards designed to (i) ensure the security and confidentiality of any non-public information (“Information”) transmitted using the Site, (ii) protect against any anticipated threats or hazards to the security or integrity of Information transmitted using the Site and (iii) protect against unauthorized access to, or use of, Information transmitted using the Site, Ingalls does not exercise any control over the Vendor’s systems and cannot guarantee the privacy and security of any information you choose to transmit using the Site.

- Access to the Site is granted by Ingalls so that you may utilize the Service for your convenience at your sole discretion. Ingalls has no liability for any loss, claim, or other damage that results from unauthorized access to any Information transmitted using the Site. User is solely responsible for the security of Information stored locally on the User’s computer or device as well as any email account User may use to receive and send links to the Site to transmit or receive documents.

3Q 2025 Investor Update

Bulls Ruled the Quarter – But Bears Have Plenty to Say

The third quarter of 2025 presented a compelling balance between economic resilience and lingering macroeconomic uncertainty. The U.S. economy grew at an impressive, annualized rate of 3.8%, supported by strong consumer spending and sustained capital investment. However, labor markets showed early signs of fatigue, with unemployment rising to a four-year high. This cooling in employment softened inflationary pressures and helped set the stage for the Federal Reserve’s first rate cut since 2020, with the Wall Street consensus expecting at least one more cut by year-end. While this policy shift buoyed investor confidence, policymakers remained cautious, with inflation still running above the target rate of 2%. The U.S. dollar weakened, providing a tailwind to exports and emerging market performance, while AI-related investment continued to accelerate, driving productivity optimism and forward-looking growth expectations.

Equity markets staged a strong rally in the third quarter, with the Standard & Poor’s 500 index posting a total return of 8.1%, driven by the ongoing AI boom and strong corporate earnings. The Information Technology sector surged by over 20%, led by standout performances from companies benefitting from chip sales, infrastructure, and software.

The "Magnificent Seven” - a small group of dominant tech names — accounted for a disproportionate share of the S&P 500’s gains. While this concentration raised some concerns about market breadth, it did not detract from the broad-based improvement in earnings across multiple sectors. Overall, corporate earnings surprised to the upside, prompting analysts to raise full-year forecasts for the S&P 500.

Another encouraging development was the renewed strength in small-cap stocks, which outperformed their large-cap peers. These companies benefited from lower interest rate expectations and increased investor appetite for domestically focused, growth-oriented opportunities. Additionally, a resurgence in IPO activity, particularly in the U.S., India, and China, reflected growing confidence in global capital markets. Investor sentiment continued to improve, as evidenced by increased flows into equity mutual funds and ETFs. The combination of supportive policy, strong earnings, and a bullish narrative around technological innovation helped reinforce risk appetite among investors.

Underneath the Hood: A Look at S&P 500 Sector Performance

Sector performance during Q3 2025 was uneven, with growth-oriented areas leading the way. Technology, Communication Services, and Consumer Discretionary were standout performers, fueled by AI adoption, digital engagement gains, and resilient consumer spending. The Fed’s rate cut provided an additional tailwind, enhancing the appeal of growth and rate-sensitive sectors. Financials benefited from improved credit conditions and steady earnings, while defensive sectors such as Consumer Staples and Healthcare lagged due to cost pressures, regulatory uncertainty, and reduced investor interest. Energy and Materials faced headwinds from lower commodity prices and tariff-related disruptions. Overall, performance reflected the market’s preference for innovation, liquidity, and earnings visibility.

What’s Ahead for Earnings?

FactSet Research Systems, our favored source for earnings data, shows analysts expect continued positive earnings momentum through the end of 2025 and into 2026. FactSet’s Earnings Insight and S&P 500 previews indicate the broad-based index is forecast to report mid-single to double-digit year-over-year earnings growth

across the coming quarters, with Q4 2025 and early 2026 quarters showing particularly strong percentage gains versus the weak comparisons from a year earlier. FactSet’s published quarter-by-quarter projections show earnings growth accelerating into 2026 after a mixed 2025, and their commentary projects mid-to high-single digit calendar-year earnings growth for 2025 overall.

What’s Driving Those Estimates?

- Base effects and revisions — Much of the near-term strength reflects easy year-ago comparisons in certain industries and analysts upward revisions where companies have reported better-than-expected results in early releases.

- Revenue and margin dynamics — FactSet’s sector reports show revenue growth across many sectors (Information Technology, Communication Services, Health Care) with margins supported by operating leverage, share buybacks, and cost discipline.

- Commodity and rates sensitivity — Earnings in Energy and Financials are being driven by commodity price moves and interest-rate dynamics respectively, creating outsized quarter-to-quarter volatility in those sectors.

The Market’s Crossroads: Understanding the Bull and Bear Divide

Markets remain caught between two powerful narratives — one of structural innovation and another of cyclical caution. Bullish investors see the rise of AI and machine learning as the foundation for a new productivity cycle capable of driving sustainable earnings growth and valuation expansion. They cite strong corporate earnings, economic resilience, monetary easing, and ample liquidity as reasons for optimism. Conversely, bearish investors warn of stretched valuations, lingering inflation, and overdependence on a narrow group of mega-cap leaders. They point to elevated P/E ratios, margin compression risks, credit stress, and geopolitical instability as warning signs of late-cycle fragility. Both camps agree that the market’s future hinges on the trajectory of inflation, policy execution, and the durability of earnings.

The Road Ahead: Keeping a Watchful Eye Out

We have long held the view that our core competency lies in the ability to identify individual opportunities with company-specific drivers. While the fluidity of economic data and events - employment trends, inflation, and credit defaults, amongst many – bear close watching, we offer a few important factors below that we look for in potential equity investments.

- Aggressive selling based on headlines, sentiment shifts, and non-fundamental reasons.

- Companies that provide “plumbing and infrastructure” supportive of trends like AI and Healthcare.

- Companies poised to benefit from prior capital expenditures on the cusp of inflecting free cash flow.

- Profit margin expansion opportunities arising from companies with pricing power and cost discipline.

- Management teams with long-term vision and “skin in the game” with significant holdings in their stock.

- Rising earnings estimates complemented by attractive valuations in out-of-favor companies.

Balancing Transformation and Caution and Remaining Disciplined

The third quarter of 2025 reaffirmed the dual nature of the current market — optimism rooted in innovation and productivity gains versus caution tied to valuations and macro risks. AI and digital transformation continue to redefine growth potential, and we believe we have taken measures over the last 18 months to ensure that we are well-positioned to benefit from these long-term trends. Historically, easing monetary conditions support risk assets, and Fed policy has started to move to a declining rate environment. Yet, inflation, fiscal uncertainty, and geopolitical volatility remain potential disruptors. As we move into the final quarter of the year and beyond, disciplined selectivity, diversified exposure, and active risk management will be critical. Our mantra of focusing on free cash flow generation, sustainable and rising profit margins, and attractive valuation are at the forefront of our strategy – as always. We believe those investors who combine conviction in structural trends with attentiveness to cyclical data will be best-positioned to navigate what remains - for now - a market balanced between transformation and temptation.

Marshall Kaplan, mkaplan@ingalls.net 212-269-0264

Rochelle Wagenheim, rwagenheim@ingalls.net 212-269-0265

Michael Nelson, mnelson@ingalls.net 212-269-9785

This presentation is to report on the investment strategies as reported by Ingalls & Snyder and is for illustrative purposes only. The information contained herein is obtained from multiple sources and believed to be reliable. Information has not been verified by Morgan Stanley Wealth Management (MSWM) and may differ from documents created by MSWM. You can obtain a copy of the MSWM Profile from your Financial Advisor. For additional information on other programs, please speak to your Financial Advisor.

The material included herein is not to be reproduced or distributed to others without Ingalls & Snyder, LLC’s (the “Firm”) express written consent. This material is being provided for informational purposes and is not intended to be a formal research report, a general guide to investing, or as a source of any specific investment recommendations and makes no implied or express recommendations concerning the manner in which any accounts should be handled. Any opinions expressed in this material are only current opinions and while the information contained is believed to be reliable there is no representation that it is accurate or complete and it should not be relied upon as such. Any investment program involves certain risks, including loss of principal, and no assurance can be given that a certain desired investment objective will be achieved.

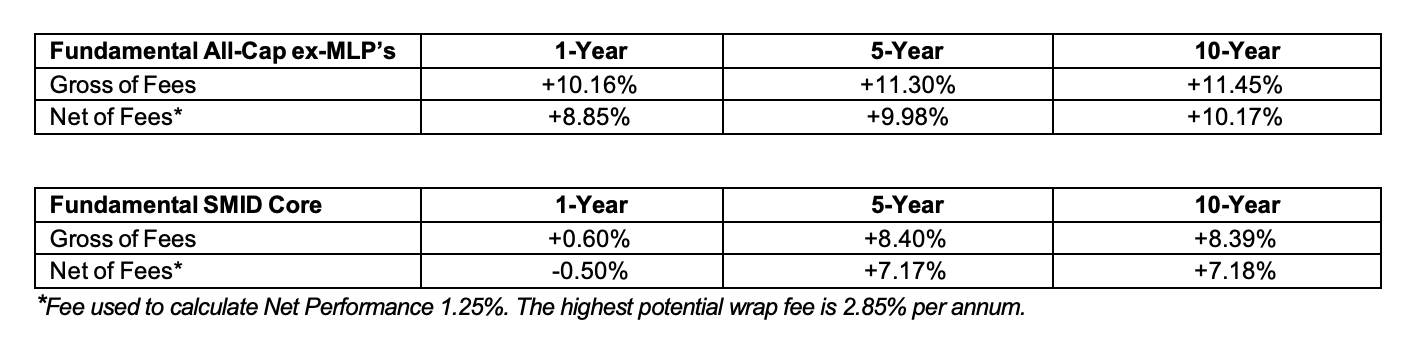

Gross returns do not reflect the deduction of any expenses. Net returns reflect returns after deduction of expenses such as charges for transaction costs, investment management/advisory fees, custody and applicable administrative expenses or wrap fees that may incorporate such expenses.

The Firm accepts no liability for loss arising from the use of this material. However, Federal and state securities laws impose liabilities under certain circumstances on persons who act in good faith, and nothing herein constitute a waiver or other limitation of any rights that an investor may have under Federal or state securities laws. For additional information about the investment manager, please refer to Form ADV Part 2.

Ingalls & Snyder is a registered investment advisor and broker-dealer based in New York City. We provide investment management and related services to private clients and institutional investors.

Check the background of this firm on FINRA's BrokerCheck