- The Site is maintained and operated by a third-party vendor, Citrix Systems, Inc. (the “Vendor”), a company that is not affiliated with Ingalls & Snyder, LLC (“Ingalls”). While Ingalls has selected the Vendor based on its belief that the Vendor has commercially reasonable safeguards designed to (i) ensure the security and confidentiality of any non-public information (“Information”) transmitted using the Site, (ii) protect against any anticipated threats or hazards to the security or integrity of Information transmitted using the Site and (iii) protect against unauthorized access to, or use of, Information transmitted using the Site, Ingalls does not exercise any control over the Vendor’s systems and cannot guarantee the privacy and security of any information you choose to transmit using the Site.

- Access to the Site is granted by Ingalls so that you may utilize the Service for your convenience at your sole discretion. Ingalls has no liability for any loss, claim, or other damage that results from unauthorized access to any Information transmitted using the Site. User is solely responsible for the security of Information stored locally on the User’s computer or device as well as any email account User may use to receive and send links to the Site to transmit or receive documents.

Technology Market Commentary

Recent turbulence in the US technology sector highlights the contrasting fortunes of different tech industries and companies. Over the past year, the performance of software and semiconductors, in particular, has diverged – and the divergence has become even more pronounced in 2026. For all the attention focused on the famous “hyper-scalers,” which provide computing infrastructure, this cohort has not performed particularly well, either.

To illustrate this point, we compare returns of three indices:

· The broad tech sector (Nasdaq), dominated by the largest firms: Alphabet, Amazon, Meta, Microsoft, Nvidia

· The software sub-sector (IGV)

· The semiconductor sub-sector (SMH)

From the beginning of 2025 through February 6, 2026 returns have been as follows:

· Nasdaq: +20.1%

· IGV (software): -17.6%

· SMH (chips): +66.4%

And year-to-date through February 6, 2026 returns have been as follows:

· Nasdaq: -0.9%

· IGV (software): -22.0%

· SMH (chips): +11.5%

Given broadly increased spending on technology, why are these different segments of technology trading so differently?

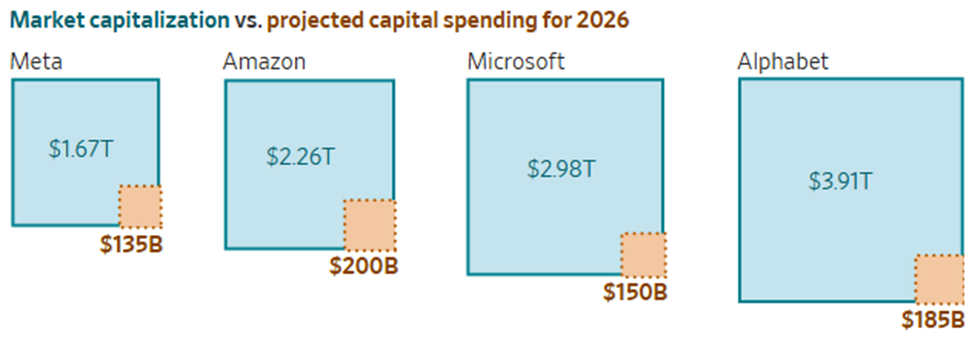

First, expectations for capital expenditure at the large cloud-computing providers are notably higher compared to just one month ago. Projected capital spending for four of the companies investing the most into datacenters is now expected to be well above $600 billion for the full year 2026. Raised capital spending forecasts have increased expectations for semiconductor demand while calling into question the return on capital for large data center projects. The Wall Street Journal recently published a graphic that captured the growing scale of capital spending at the 4 major cloud-computing providers:

Second, a large portion of this massive capital expenditure supports growth in artificial intelligence workloads. Two recent releases out of the leading AI labs, Anthropic and OpenAI, have targeted automation of knowledge work. The capabilities are impressive and include the ability to build some applications without coding knowledge.

These tools from Anthropic (“Claude Cowork”) and Open AI (“Codex”), have led to multiple concerns for software companies:

1. Existing software can now be replaced relatively easily

2. AI-driven automations will decrease the need for human labor, lead to layoffs, and drive down the number of seat-based licenses companies need to purchase

3. existing software will be “abstracted away” by AI tools, leading to reduced pricing power and revenue growth for incumbents.

While software appears at risk of being devoured by AI tools, shortages of chips required for data centers ensure strong pricing power and margins for chip-makers. These companies generally show extended order backlogs. Additional memory-chip capacity, for instance, won’t become available until late 2027.

The expanding scope of AI data-center investment – and the speed at which the leading AI labs innovate and launch competitive offerings – weighs on the valuations of most software stocks. Yet the recent collapse in their share prices attracts our interest, particularly as the above concerns have been well-flagged by now. In our view, the supposed dichotomy between software applications and AI-based tools is misleading. As the software industry learns to integrate AI, selective investment situations may prove rewarding, especially in light of historically low valuations.

The material is not to be reproduced or distributed to others without Ingalls & Snyder, LLC’s (“Ingalls” or the “Firm”) express written consent. This material is being provided for informational purposes and any opinions expressed in this material are only opinions at the time of writing. Nothing provided by Ingalls should be considered tax or legal advice, and clients should seek advice from their tax and legal professionals. Bridgehampton is a team at Ingalls & Snyder, LLC, an investment advisor registered with the Securities & Exchange Commission and a FINRA member broker dealer. More information including the firm’s Form ADV Brochure and Form CRS can be found at https://www.ingalls.net/importantinformation.

Ingalls & Snyder is a registered investment advisor and broker-dealer based in New York City. We provide investment management and related services to private clients and institutional investors.

Check the background of this firm on FINRA's BrokerCheck