- The Site is maintained and operated by a third-party vendor, Citrix Systems, Inc. (the “Vendor”), a company that is not affiliated with Ingalls & Snyder, LLC (“Ingalls”). While Ingalls has selected the Vendor based on its belief that the Vendor has commercially reasonable safeguards designed to (i) ensure the security and confidentiality of any non-public information (“Information”) transmitted using the Site, (ii) protect against any anticipated threats or hazards to the security or integrity of Information transmitted using the Site and (iii) protect against unauthorized access to, or use of, Information transmitted using the Site, Ingalls does not exercise any control over the Vendor’s systems and cannot guarantee the privacy and security of any information you choose to transmit using the Site.

- Access to the Site is granted by Ingalls so that you may utilize the Service for your convenience at your sole discretion. Ingalls has no liability for any loss, claim, or other damage that results from unauthorized access to any Information transmitted using the Site. User is solely responsible for the security of Information stored locally on the User’s computer or device as well as any email account User may use to receive and send links to the Site to transmit or receive documents.

Investor Update, May 2026

2026 year-to-date highlights:

- Equity markets more than recovered March declines

- S&P 500 +5.3% year-to-date – despite declining by 9% in March

- Leadership narrowed to semiconductors & energy

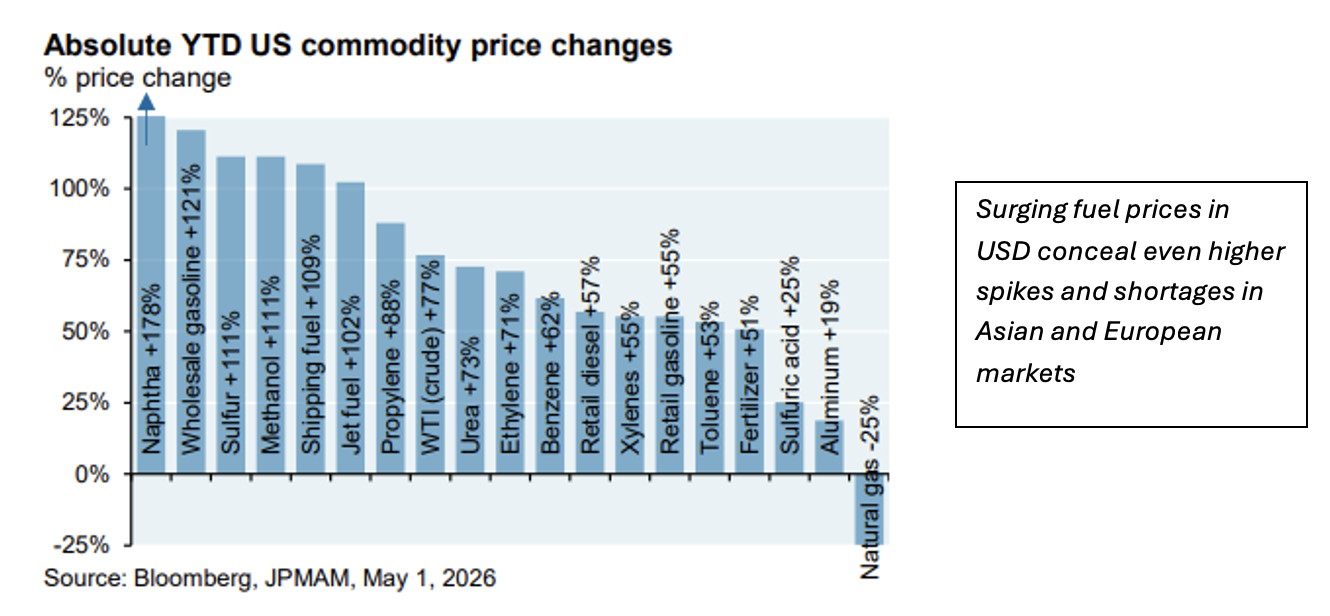

- Surging prices of energy and materials

- Petroleum & derivative products +50-200%

- Semiconductors +49% on AI demand – see discussion below

- Few hedges against inflation risk

- Gold, high-grade bonds, defensive stocks modestly down year-to-date

Energy prices & AI

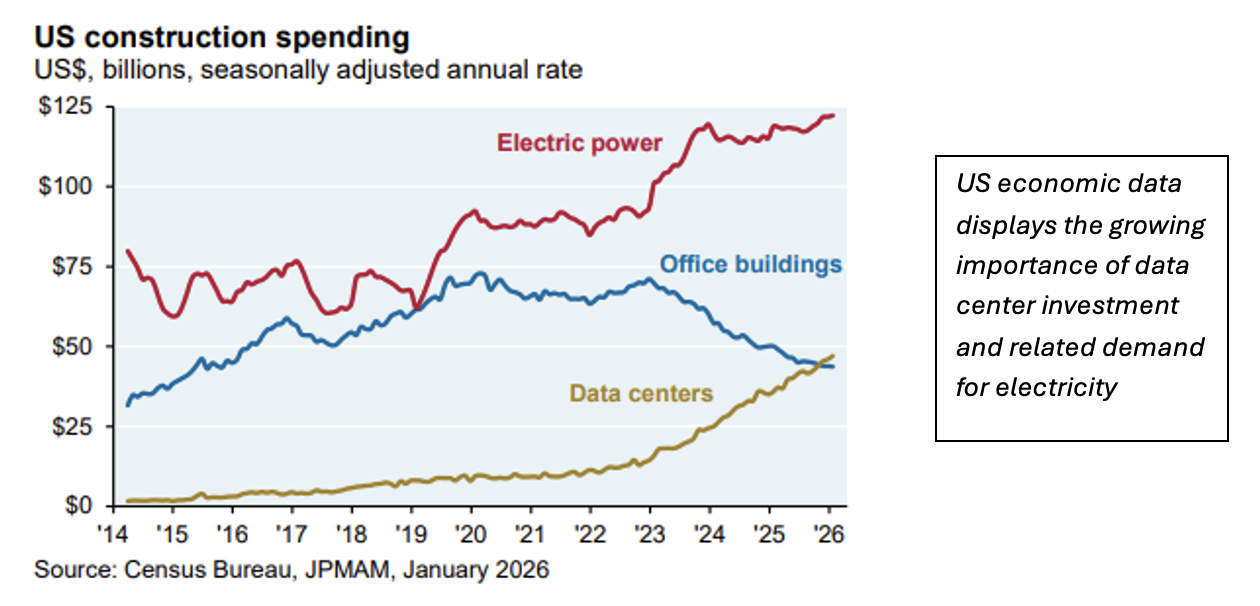

The energy price shock driven by war in the Middle East coincides with surging AI-driven demand for semiconductors and related materials. The oil and semiconductor price surges are related: they both involve severe constraints on natural resources, materials and logistics. Note that energy prices began to climb in early 2026 (before the Iran war) as markets priced the rising impact of data-center demand. This demand spurs capital spending on a historic scale. At approximately $800 billion on an annual basis, US data-center capital investment is equivalent to 2.5% of GDP, and accounts for the majority of US GDP growth.

The imperative for the US to dominate AI – both in competition with China and for global security reasons – encourages a search for affordable, abundant energy. This quest for resources encompasses OPEC+ countries such as Venezuela and Iran. Possibly, this AI energy imperative has contributed to geopolitical frictions given the likely proliferation of AI globally, both in civilian and military spheres.

Perspective on AI & data-center demand

The soaring growth displayed by data center suppliers, particularly chip makers, paused only briefly during the outbreak of war in March. AI-related businesses lead the US and global equity markets and account for the bulk of positive revisions to earnings forecasts. Historically, the capital-intensive and highly-cyclical semiconductor industry has tended to provide trading opportunities rather than long-term investment gains. One could have called time on this rally back in 2024 or in late 2025 (Microsoft, one of the largest providers of computing power, pulled back on its spending plans in early 2025 – before quickly reversing course). The current surge in chip-maker share prices is now in its 3rd year; yet the major players continue to post impressive growth in profits. While demand from US data center operators surges, there is little spare chip capacity available before 2028—and even that additional capacity may not be sufficient to meet demand levels in two years’ time. Unsurprisingly, prices for all chips and related components, even the most basic, have surged in recent months.

Our own views on the semiconductor “supercycle” continue to evolve. In recent months, attention has shifted from graphic processing units (GPUs), vital to the creation of large-language models (LLMs), including ChatGPT, Gemini and Claude, to the growing role of central processing units (CPUs) in supporting AI inference tasks. Optical networking and AI-enabled devices have also emerged as high-growth segments. This new phase of AI demand will likely favor a different set of suppliers. Despite the frenzied rise in prices of certain stocks, we should view AI as a long game.

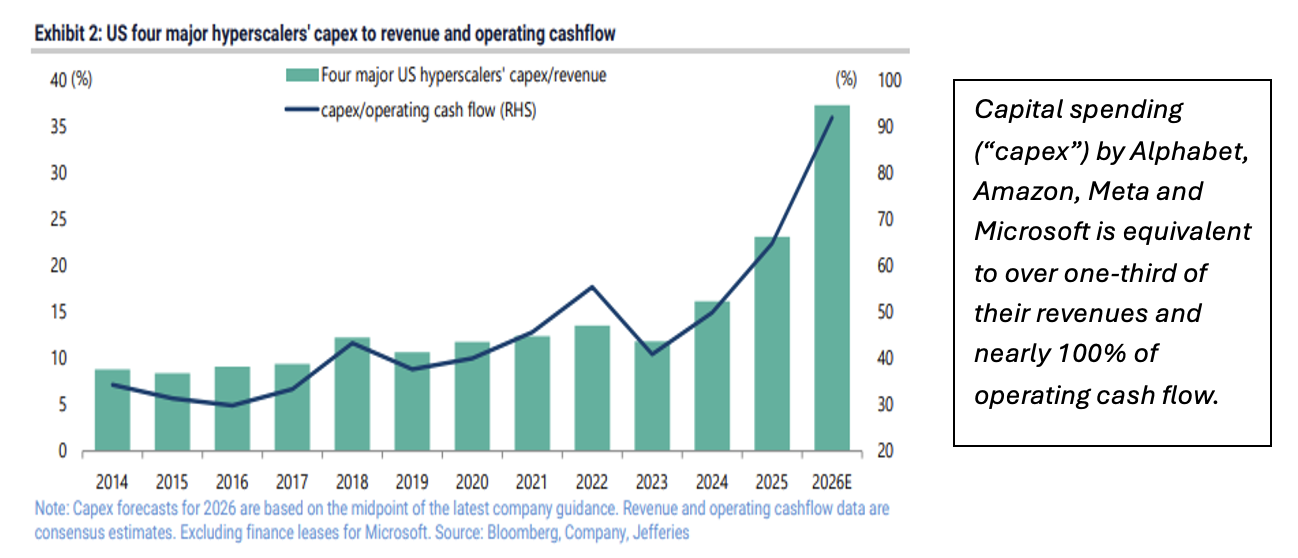

The “hyperscalers,” i.e., the largest data center operators, remain dominant in the competitive landscape and in the stock market. Each of them is valued at well over $1 trillion. Yet the financial profiles of these gigantic companies appear very different today compared to only 2 years ago.

As their financial profiles shift from high free-cash-flowing, asset-light digital services to more capital-intensive infrastructure providers, their stock market performance has lagged that of the semiconductor group – with the notable exception of Alphabet. We should note that it is hardly unprecedented for suppliers to outperform their much larger customers (jet engine suppliers and aircraft makers are a salient example).

We should also be mindful of the growing concentration of hyperscaler customer bases, as Anthropic and OpenAI drive a large share of overall demand for data center capacity. Both companies closed funding rounds which valued them at $800-900 billion; both expect to offer shares to the public later this year. The sustainability of the AI infrastructure build-out increasingly hinges on the successful public listings of Anthropic, OpenAI, and other AI native “unicorns.” These potentially giant IPOs would provide much-needed liquidity to these young companies. And they will determine to a great extent whether the hyperscale players can maintain their current capex velocity without further compressing their free-cash-flow profiles.

The investment case for massive infrastructure spending today rests on cash flow generated tomorrow. The criticism often levelled at the mega-cap tech stocks tends to focus on the uncertainty of this future cash flow. Yet the hyperscalers remain well-positioned to benefit not only from future revenue but from future productivity gains. It may well be that the truly powerful and lucrative adoption phase of AI coincides with a substantial decrease in the cost of supplies and operations. Alternatively, the market action in semiconductor stocks suggests that productivity gains from AI would justify current infrastructure investments, even at much higher input costs than we see today.

Perspectives on war & energy prices

The war in the Middle East (and Ukraine) will have repercussions well beyond the present moment. Infrastructure will need to be rebuilt, while countries and corporations at risk of shortages race to secure new sources of supply. We cannot be certain of a favorable near-term outcome. Nor can we be sure that fertilizer and energy prices will soon collapse in time to provide relief to inflation-weary consumers. By the same token, we consider increasingly likely a scenario in which petroleum demand will adapt as buyers seek alternatives both to oil generally, and particularly to the kind produced in the Middle East and delivered via the Strait of Hormuz. Securing supplies, building redundant stocks and improving the efficiency of energy consumption will have risen on the priority list for nations and for corporations.

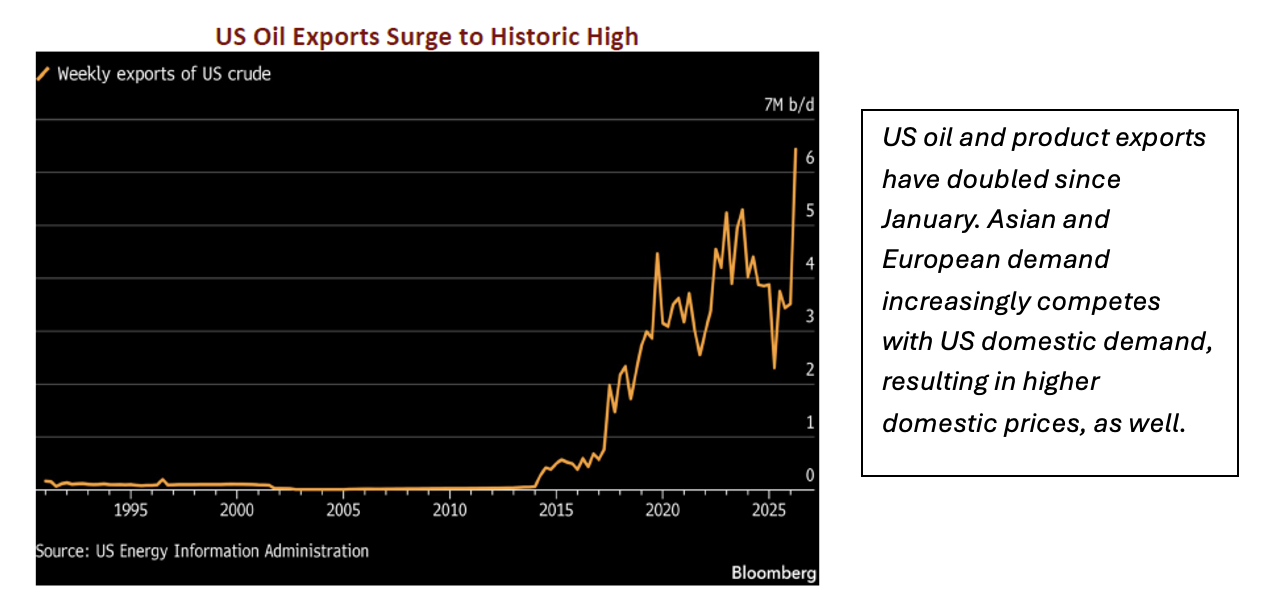

The dramatic rise in energy exports from the US reflects what may turn out to be a long-term shift in global energy supply:

In the context of explosive power demand from data centers, and heightened competition with China for resources, US efforts to break the OPEC cartel and open supply channels makes strategic sense. Whether the present war in Iran is the best means of achieving that goal is open to question.

We are grateful for the confidence you have placed in our abilities. We welcome your observations and questions, as always.

Sincerely,

Bridgehampton Group

For questions or follow-up, please reach out to any member of our team. https://www.ingalls.net/bridgehamptongroup/about-us

Ingalls & Snyder, LLC, is an investment advisor registered with the U.S. Securities & Exchange Commission and a FINRA member broker dealer. This material is being provided to you for informational purposes only and is not intended to be a general guide to investing, or as a source of any specific investment recommendation and makes no implied or express recommendation concerning the manner in which any account should be handled. Any investment program involves certain risks, including loss of principal, and no assurance can be given that any specific investment objective will be achieved.

Ingalls & Snyder is a brand name used by affiliated companies of I&S Group, LLC. Brokerage services are offered through Ingalls & Snyder, LLC (“INGS”), a FINRA and SIPC member, and advisory services are offered through Ingalls Investment Management, LLC (“IIM”), an SEC-registered investment adviser. Individuals provide brokerage services as registered representatives of or associated persons of INGS, and advisory services as investment adviser representatives or employees of IIM.

For more information and disclosures regarding INGS and IIM , please visit the Important Information page. In addition, you may check INGS’ regulatory history and background on FINRA’s BrokerCheck website.

Check the background of this firm on FINRA's BrokerCheck